版權說明:本文檔由用戶提供并上傳,收益歸屬內容提供方,若內容存在侵權,請進行舉報或認領

文檔簡介

1、Fiscal Risks Paolo Mauro Fiscal Affairs Department International Monetary Fund Introduction Fiscal Risks: Deviations of fiscal outturns (deficits, debt/GDP) from expectations at the time of the budget or other fiscal forecasts. How large and frequent are the deviations for different groups of countr

2、ies? What are the most important types of shocks? Does this depend on degree of integration in global financial markets? (Will rely on work on the correlates of output drops.) What can policy makers do about fiscal risks? (Identify, Disclose, Manage). Statements of Fiscal Risks. Begin by looking at

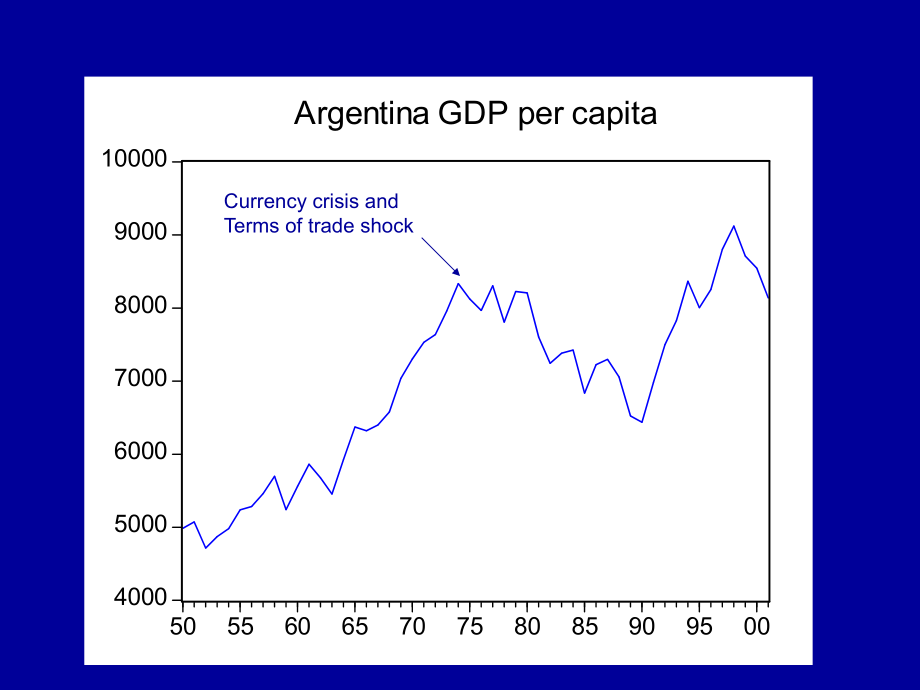

3、Output Drops Definition of output drop Frequencies Catalog of shocks Unconditional and conditional frequencies, expected cost Bivariate, then multivariate (probit) approach Causality (timing)400050006000700080009000100005055606570758085909500Argentina GDP per capitaCurrency crisis andTerms of trade

4、shockTable 2. Output Drops: Frequency, Duration and Loss, 1970-2001Source: Authors calculations based on Maddison (2003) data.Notes: “All” output drops include concluded, ongoing and sub-events. Concluded drops are fully observed within the sample period whereas ongoing drops had not ended by 2001 a

5、nd the duration and loss for these drops are calculated assuming that the drops ended in 2002. Expected cost = = unconditional probability of a shock probability of output drop given the shock cost of the output drop when it occursFigure 2. Expected Cost of Shocks Based on Bivariate Estimates(in per

6、cent of pre-event GDP per capita) Figure 2b. Ex-ante Cost of Shocks Based on Multivariate Estimates that are Statistically Significant(in percent of pre-event GDP per capita) Output Drops and Shocks: Key Results 1900-2001 and four sub-periods: countries with lower initial p/c incomes have more outpu

7、t drops. 1970-2001: emerging markets have a drop every 16 years, duration 6 years, cumulative cost 40% of a years GDP; developing countries twice the costs Financial shocks matter more for emerging markets, real shocks for developing countries. For given output drop, decline in consumption is lower

8、in countries that are at high level of financial development than in countries of medium and low levels of financial development. Output Drops are All Unexpected: Forecast Error from October One Year Ahead 024681012-20-15-10-50Series: WEO_DACTOCTSample 1900 2001 IF EVENT_ALL25Observations 40Mean -5.

9、648995Median -4.819912Maximum 1.470343Minimum -19.32673Std. Dev. 4.640448Skewness -0.803957Kurtosis 3.562790Jarque-Bera 4.836862Probability 0.089061Now move to Fiscal Risks Fiscal Risks: Deviations of fiscal outturns (deficits, debt/GDP) from expectations at the time of the budget or other fiscal fo

10、recasts. Possible sources: macroeconomic shocks (exchange rate, cost of borrowing,.), contingent liabilities (guarantees, PPPs), legal claims against the government, bailouts of local governments, state-owned enterprises, banks, assumptions of debts. How large and frequent Preliminary empirical work

11、 on sources of risksAll Countries-Surprise Deviations in Debt/GDP10th Percentile020406080100120140Frequencymean-1sd+1sd-2sd+2sd-3sd+3sd-4sd+4sd-5sd+5sd -30-20-100102030In percent of GDP; positive deviation if actual forecastTotal obs. 398; mean=-0.77; sd=6.78; skewness=0.21; kurtosis=6.96Deviations

12、of Debt/GDP-All Countries Surprise Deviations in Debt/GDP10th percentile01020304050607080Frequencymean-1sd+1sd-2sd+2sd-3sd+3sd-4sd+4sd-5sd+5sd -30-20-100102030In percent of GDP; positive deviation if actual forecastTotal obs. 257; mean=-0.03; sd=5.73; skewness=0.19; kurtosis=5.60Advanced Countries 1

13、0th Percentile01020304050Frequencymean-1sd+1sd-2sd+2sd-3sd+3sd-4sd+4sd -30-20-100102030In percent of GDP; positive deviation if actual forecastTotal obs.73; mean=-1.88; sd=8.62; skewness=0.80; kurtosis=7.52Emerging Countries10th Percentile051015202530Frequencymean-1sd+1sd-2sd+2sd-3sd+3sd-4sd+4sd -30

14、-20-100102030In percent of GDP; positive deviation if actual forecastTotal obs. 68; mean=-2.38; sd=7.81; skewness=-0.02; kurtosis=5.44Developing Countries All Countries- Surprise Deviations in Balance/GDP10th Percentile04080120 160 200 240 280 320Frequencymean-1sd+1sd-2sd+2sd-3sd+3sd-4sd+4sd-5sd+5sd

15、-6sd+6sd -20-15-10-505101520In percent of GDP; positive deviation if actual forecastTotal obs. 1397; mean=-0.36; sd=3.21; skewness=-0.47; kurtosis=8.96Deviations of Balance/GDP-All Countries Surprise Deviations in Balance/GDP10th Percentile0102030405060708090100Frequencymean-1sd+1sd-2sd+2sd-3sd+3sd-

16、4sd+4sd-5sd+5sd -10-50510In percent of GDP; positive deviation if actual forecastTotal obs. 378; mean=0.02; sd=2.20; skewness=-0.42; kurtosis=6.80Advanced Countries10th percentile020406080100120140Frequencymean-1sd1sd-2sd2sd-3sd3sd-4sd4sd-5sd5sd-6sd6sd -20-15-10-505101520In percent of GDP; positive

17、deviation if actual forecastTotal obs. 388; mean=-0.57; sd=3.52; skewness=-0.66; kurtosis=10.34Emerging Countries 10th Percentile020406080100120140160Frequencymean-1sd+1sd-2sd+2sd-3sd+3sd-4sd+4sd-5sd+5sd -15-10-5051015In percent of GDP; positive deviation if actual forecastTotal obs. 631; mean=-0.45

18、; sd=3.49; skewness=-0.21; kurtosis=6.86Developing Countries Adverse Terms of Trade Shock(worsening of the terms of trade for goods by 10 percent or more)10th percentile01020304050Frequencymean-1sd+1sd-2sd+2sd-3sd+3sd-4sd+4sd -20-15-10-5051015In percent of GDP; positive deviation if actual forecastT

19、otal obs. 128; mean=-1.15; sd=4.10; skewness=-0.92; kurtosis=6.85Deviations of Balance/GDP-All CountriesCurrency Crises(depreciation by at least 25 p.p. and at least 10 p.p. greater than the previous year)10th percentile051015Frequencymean-1sd+1sd-2sd+2sd-3sd+3sd -10-50510In percent of GDP; positive

20、 deviation if actual forecastTotal obs. 46; mean=-2.22; sd=3.33; skewness=-0.91; kurtosis=3.12Deviations of Balance/GDP-All CountriesBanking Crises(outbreak years of crises as identified in the literature)10th percentile051015Frequencymean-1sd+1sd-2sd+2sd-3sd+3sd-4sd+4sd -10-50510In percent of GDP;

21、positive deviation if actual forecastTotal obs. 35; mean=-1.05; sd=2.75; skewness=-0.31; kurtosis=2.97Deviations of Balance/GDP-All CountriesSudden Stops(worsening of financial balance by more than 5 p.p. of GDP)10th percentile010203040506070Frequencymean-1sd+1sd-2sd+2sd-3sd+3sd-4sd -20-15-10-505101

22、5In percent of GDP; positive deviation if actual forecastTotal obs. 154; mean=-0.62; sd=4.85; skewness=-0.56; kurtosis=5.99Deviations of Balance/GDP-All Countries Oil Exporters: Years of Oil Price increase05101520Frequencymean-1sd+1sd-2sd+2sd-3sd+3sd-4sd4sd-30-20-10010203040In percent of GDP; positi

23、ve deviation if actual forecastTotal obs. 27; mean=-6.07; sd=10.23; skewness=-0.70; kurtosis=2.94Deviations of Debt/GDP-Fuel Exporters0369121518Frequencymean-1sd+1sd-2sd+2sd-3sd+3sd-15-10-505101520In percent of GDP; positive deviation if actual forecastTotal obs. 26; mean=3.16; sd=5.18; skewness=-0.41; ku

溫馨提示

- 1. 本站所有資源如無特殊說明,都需要本地電腦安裝OFFICE2007和PDF閱讀器。圖紙軟件為CAD,CAXA,PROE,UG,SolidWorks等.壓縮文件請下載最新的WinRAR軟件解壓。

- 2. 本站的文檔不包含任何第三方提供的附件圖紙等,如果需要附件,請聯系上傳者。文件的所有權益歸上傳用戶所有。

- 3. 本站RAR壓縮包中若帶圖紙,網頁內容里面會有圖紙預覽,若沒有圖紙預覽就沒有圖紙。

- 4. 未經權益所有人同意不得將文件中的內容挪作商業或盈利用途。

- 5. 人人文庫網僅提供信息存儲空間,僅對用戶上傳內容的表現方式做保護處理,對用戶上傳分享的文檔內容本身不做任何修改或編輯,并不能對任何下載內容負責。

- 6. 下載文件中如有侵權或不適當內容,請與我們聯系,我們立即糾正。

- 7. 本站不保證下載資源的準確性、安全性和完整性, 同時也不承擔用戶因使用這些下載資源對自己和他人造成任何形式的傷害或損失。

最新文檔

- 社區服務與鄰里關系考核試卷

- 融資租賃業務中的客戶信用風險管理考核試卷

- 初中校園文化建設工作計劃

- 雙減背景下小學2024-2025學年課外活動管理計劃

- 小學環境保護教育課程教學計劃

- 2025年醫院醫保改革實施計劃

- 企業美術培訓員工發展計劃

- 2025春廣東開放大學《學習指引(本專)》學習心得與行為評價

- 小學四年級親子音樂活動計劃

- 廣西城市職業大學《大型數據庫應用實訓》2023-2024學年第二學期期末試卷

- 熱點主題作文寫作指導:古樸與時尚(審題指導與例文)

- 河南省洛陽市2025屆九年級下學期中考一模英語試卷(原卷)

- 2025年入團考試各科目試題及答案分析

- 電網工程設備材料信息參考價2025年第一季度

- 江蘇南京茉莉環境投資有限公司招聘筆試題庫2025

- 2024年安徽省初中學業水平考試生物試題含答案

- 2024年浙江省中考英語試題卷(含答案解析)

- MOOC 理解馬克思-南京大學 中國大學慕課答案

- 說明書hid500系列變頻調速器使用說明書s1.1(1)

- ISO22716:2007標準(中英文對照SN T2359-2009)47

- RTO處理工藝PFD計算

評論

0/150

提交評論